800-503-2102

800-503-2102

Should I Talk to Uber’s Insurer or Get a Lawyer First? Your Options Explained

Key Takeaways:

- Speaking to Uber’s insurer too soon or without preparation can reduce the value of your claim—it’s important to understand your rights and gather key information first.

- Rideshare accident claims are complex, with insurance coverage depending on the driver’s app status and fault; knowing these details helps protect your interests.

- ZAF Legal’s free AI assistant lets you assess your case, estimate its value, and decide whether to handle your claim yourself or with a lawyer—empowering you to choose the right level of support.

Insurance adjusters are trained to settle claims for as little as possible — and they may reach out before you’ve even left the hospital. When you’re already calculating ambulance bills and missed shifts, a single misstep can quietly shrink your settlement. Consumer insurance guidelines confirm that insurers can request recorded statements.

Rideshare crashes add another layer to this decision — coverage depends on what trip phase the driver was in. ZAF’s free AI assistant helps you see whether you have a case, what it might be worth, and whether a lawyer would net you more.

Should I Talk to Uber’s Insurance Company Right Away?

After an Uber crash, insurance adjusters often start calling within hours — sometimes before you’ve even had a chance to see a doctor. The pressure to respond can feel immediate, but knowing what you’re actually required to do helps protect your claim from the start.

Do I have to speak with an adjuster immediately, or can I wait?

No, you are not required to give a detailed statement right away. You can confirm the accident happened without discussing fault, injuries, or what you think caused the crash. Taking time to get your bearings before an in-depth conversation is your right.

Should I give a recorded statement when I’m still in pain or unsure of my injuries?

In most cases, it’s best to wait. Delayed symptoms like neck pain or concussion signs can take days to appear. Giving a recorded statement too soon can commit you to details that don’t yet reflect your actual injuries and that can affect your claim.

What should I have ready before speaking with Uber’s insurer?

Before any detailed conversation, gather what you can — the trip receipt, driver information, photos from the scene, and a copy of the police report. Basic identifying information is fine to confirm. The NAIC recommends keeping a written record of every communication with adjusters from the start.

Can saying “I’m okay” or guessing about fault hurt my claim?

It can. Adjusters are trained to document everything you say, and a casual “I’m fine” can be used to minimize your injuries later. Guessing about fault — even partially — can reduce what you’re owed in states where being even partly responsible for the crash lowers your payout.

What should I do if Uber’s insurer keeps calling or texting?

You can respond briefly to confirm you received their message without committing to a recorded statement or in-depth conversation. If calls feel aggressive or high-pressure, you have the right to file a complaint with your state’s insurance regulator. Before deciding how to respond, ZAF’s free AI assistant can help you understand where you stand.

How Does a Rideshare Insurance Claim Work After an Uber Crash?

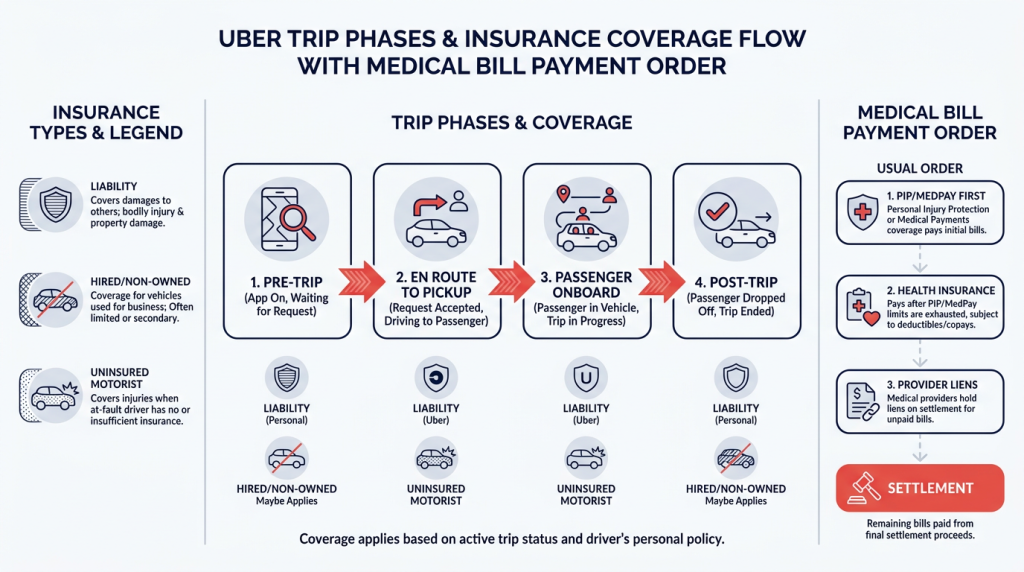

After an Uber accident, most people aren’t thinking about insurance phases. They’re wondering whether the ambulance ride just created a bill they can’t pay. What coverage applies — and who handles your medical bills — depends on a single detail: what the driver was doing when the crash happened.

Who actually pays after an Uber accident?

It depends on who was at fault and what the driver was doing at the time. If another driver caused the crash, their insurer is usually first in line. If the Uber driver was at fault, either their personal insurer or Uber’s commercial coverage may apply. This breakdown explains how liability works in more detail.

Does it matter what the Uber driver was doing when the crash happened?

Yes — this is one of the most important details in any rideshare insurance claim. Uber’s coverage shifts across three phases: driver offline, driver waiting for a ride request, and driver en route or carrying a passenger. When a passenger is on board, Uber carries up to $1 million in liability — though exact limits can differ by state.

What documents should I pull together before talking to any insurer?

Start with your in-app trip receipt, the driver’s name, vehicle details, and any police report number. Photos of vehicle damage and visible injuries help establish what happened before details fade. File a crash report through the Uber app, too — the sooner, the better. Having all of this ready means you’re working from facts, not memory.

How do medical bills get paid while my claim is still open?

If you have PIP or MedPay coverage, that pays first. Your health insurance picks up what’s left though it may later seek reimbursement from the at-fault insurer. If neither applies, many providers will treat you now and be paid from your settlement later — so you owe nothing upfront. How your state handles this can affect the order.

Can I keep seeing a doctor without paying out of pocket right now?

In most cases, yes. PIP, health insurance, or a provider lien arrangement means most accident victims can receive full care without paying anything upfront. Gaps in treatment can be used to argue your injuries weren’t serious — so staying consistent matters for your health and your claim.

Would an Uber Accident Lawyer First Help More Than Handling It Myself?

Deciding whether to get an Uber accident lawyer first, or handle things yourself, is one of the most important choices after a crash. The right answer depends on your situation, but there are honest patterns worth knowing before you decide.

When does it make sense to get a lawyer before talking to Uber’s insurer?

When injuries are more than minor, fault is disputed, or multiple insurance policies are involved, getting an Uber accident lawyer first makes sense. Adjusters work for the insurer, not for you. Understanding your position before that conversation can help you avoid saying something that unintentionally reduces your claim’s value. ZAF’s explainer on your rights after an Uber crash covers this in more detail.

Will hiring a lawyer actually get me more money after their fees?

For most valid injury claims, yes. Research on attorney representation consistently shows that legal counsel tends to increase compensation, even after fees. Studies tracking road traffic claims also show lawyer involvement has grown steadily over time. That pattern reflects how often representation leads to meaningfully higher settlements.

Are there situations where handling an Uber accident claim myself is realistic?

It’s possible in limited situations: if your injuries were genuinely minor, treatment is complete, and fault is straightforward. Most people with valid injury claims still walk away with more in their pocket when they have representation. It’s worth understanding that tradeoff clearly before choosing the DIY path.

What does a contingency fee mean — and will I really pay nothing upfront?

A contingency fee means your attorney only gets paid if you win or settle your claim. There are no upfront costs and no bills while your case is active. At ZAF Legal, full-service representation works exactly this way. If you start with the DIY bundle (~$49.99) and later switch to full-service, that payment is refunded.

What can ZAF’s AI assistant help me figure out before I decide?

ZAF’s free AI assistant helps you understand whether you have a case and what it might be worth. It also helps you see whether an attorney is likely to get you a better result. You can then choose free AI guidance, a DIY bundle (~$49.99) with an attorney consultation, case summary, and Claims Coach course, or full-service representation. Full-service has no upfront fees, and the bundle cost is refunded if you switch.

Get Clarity Before You Talk to Uber’s Insurer

Speaking with an insurer before you understand your position can affect what your Uber accident claim is worth. How rideshare coverage works depends on the driver’s app status at the time of the crash. Those details determine which insurer is responsible and how much coverage is available.

ZAF Legal’s free AI assistant helps you understand whether you have a case and what it might be worth. It also helps you see whether an attorney would likely net you more.

Before you respond to Uber’s insurer, understand your Uber accident options with ZAF’s AI assistant, available 24/7 with no signup required. Whichever direction feels right, there’s a path for it: free AI guidance, a DIY bundle starting around $49.99 (refunded if you switch to full service), or full-service attorney representation with zero upfront attorney fees. Keep in mind that ZAF’s AI provides legal information and guidance — legal advice comes from licensed attorneys.

Disclaimer: This content is for informational purposes only and does not constitute legal advice, and reading the content does not create an attorney-client relationship.