800-503-2102

800-503-2102

What Is the Average Uber Accident Settlement Amount in 2026?

Key Takeaways:

- Uber accident settlement amounts vary widely and depend on injury severity, insurance coverage, and fault—not on misleading online averages.

- Thorough documentation of medical care, lost wages, and liability evidence is crucial for maximizing your settlement, whether you negotiate yourself or work with an attorney.

- ZAF Legal’s AI-powered assistant empowers accident victims to understand their claim value, organize their case, and choose between DIY negotiation, free attorney consultation, or full legal representation—all with zero upfront fees.

Uber accident settlement amounts can range from a few thousand dollars to over a million, which makes any single “average” meaningless for your case. The truth is that settlement values depend on injury severity, fault determination, and insurance coverage limits rather than industry averages you might find online. Your specific situation matters far more than someone else’s case in another state.

What matters more than any average is understanding your unique situation and the factors you can actually control. Documenting your medical care, tracking lost wages, and building a clear liability case will position you for a fair Uber accident settlement amount on average without worrying about upfront legal fees or intimidation. ZAF Legal helps accident victims understand where they stand and build a strong case summary, whether you choose to handle negotiations yourself or connect with an experienced attorney.

What Actually Drives Uber Accident Settlement Amounts

Settlement amounts aren’t based on online averages or how upset you are about the accident. The factors influencing Uber accident settlement amount come down to documented injury severity, available insurance coverage, and the strength of your liability case. Understanding these concrete elements gives you more control over your outcome than chasing misleading settlement averages.

Medical records and treatment consistency matter most.

Your medical records and treatment consistency carry far more weight than any settlement average you find online. Insurance adjusters review your emergency room visit, follow-up appointments, imaging results, and treatment gaps to determine injury severity. Government compensation programs use similar approaches, requiring thorough medical proof and consistent care records to calculate awards. Skipping recommended physical therapy or avoiding a specialist referral can reduce offers significantly. If cost concerns are keeping you from follow-up care, document the recommended treatment and explore payment plans or medical liens rather than creating gaps in your file. Ultimately, the nature and extent of your injuries determines the size of your case, and the way you prove the nature and extent of your injuries is through medical bills, records, and reports.

Beyond medical records, the timing of your accident also matters for coverage limits.

Uber’s insurance operates differently depending on the driver’s app status when the accident occurred. When the app is offline, the driver’s personal insurance typically applies with standard policy limits. Once the app is active or a ride is accepted, higher coverage limits usually become available, but policy limits can still restrict what you recover. Even in cases with clear liability and severe injuries, available coverage caps can limit your maximum settlement.

Finally, fault determination and evidence quality drive negotiations.

If you’re found partially at fault, your settlement gets reduced by that percentage in most states. These fault rules vary by state, but documented evidence of the other party’s negligence strengthens your position more than emotional arguments. Police reports, witness statements, photos, and traffic camera footage create the foundation for liability arguments. A well-organized evidence package with clear proof typically moves settlement offers more effectively than threats or pressure tactics. More often than not, the investigating officer’s report will carry the day on making a liability determination.

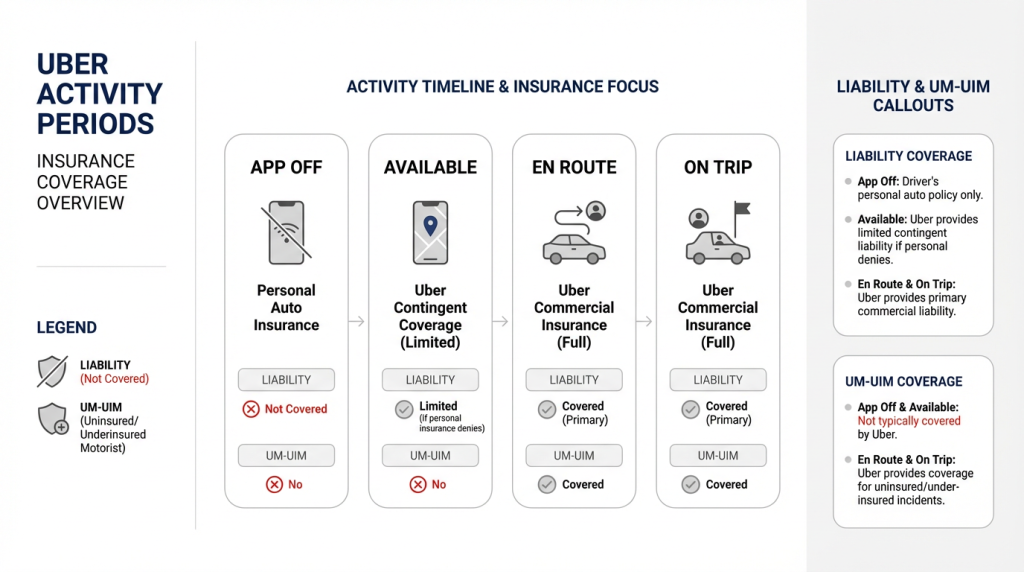

Understanding Uber’s Insurance Periods And Why They Matter

The amount of insurance coverage available for your claim largely depends on what the Uber driver was doing when the accident happened. Uber’s insurance (Uber’s official driver insurance information) operates in four distinct periods, each with different coverage limits that can directly impact your settlement amount.

| Period | Whose Insurance Applies | Typical Coverage Focus | Notes |

|---|---|---|---|

| App Off | Driver’s personal auto policy | Standard personal coverage limits | Personal policy may exclude rideshare activity |

| App On (Available) | Uber backup coverage | $50,000/$100,000/$25,000 | Lower limits; driver’s policy primary |

| En Route to Pickup | Uber primary liability | $1,000,000 per incident | Full commercial coverage begins |

| On Trip | Uber primary liability | $1,000,000 per incident | Highest protection period |

Coverage jumps significantly once a ride request is accepted, which explains why the timing of your accident matters so much for potential recovery. Some states also provide uninsured motorist coverage during certain periods, though availability varies by location and specific policy terms. Understanding which coverage applies can help you know what resources are available to cover your medical bills and lost wages.

How Claims Are Valued: Bills, Lost Wages, And Pain & Suffering

Economic damages form the foundation of how Uber accident settlements are calculated. These include every medical bill from your ER visit to physical therapy, lost wages from missed shifts, and out-of-pocket costs like prescription medications or transportation to appointments. That ambulance ride you’re worried about paying for becomes part of your recoverable damages, not an additional burden. Adjusters add up these documented expenses first, so keep every receipt, bill, and pay stub. One of the advantages to hiring a lawyer early on is they will make sure all of these expenses are documented, and you can just focus on your treatment.

Non-economic damages cover pain, suffering, and how the injury affects your daily life. When trying to calculate a fair number for general damages, people often use multiplier methods, taking your medical bills and multiplying by a factor based on injury severity and recovery time. Consistent medical treatment strengthens this calculation, but gaps in care can reduce offers significantly. If cost is preventing you from seeing that specialist or attending physical therapy, ask providers about payment plans or note the financial barrier in writing rather than skipping care entirely.

Negotiating Your Uber Accident Settlement: DIY Or With A Lawyer

Once you understand what drives settlement amounts, the next question becomes whether you can negotiate your Uber accident settlement without a lawyer or if you need professional help. The answer depends on your case complexity, injury severity, and comfort level with the process.

Building A Strong Demand Package

Your negotiation starts with a structured demand letter that presents your case clearly and professionally. This package should include several key components: a liability summary explaining how the accident happened, a chronological medical timeline showing your treatment, proof of lost wages with pay stubs or employer letters, photos of vehicle damage and injuries, and a specific settlement amount with supporting reasoning. Demand letter experts at Nolo emphasize that insurance adjusters respond better to well-documented cases than emotional appeals or threats. ZAF’s AI assistant can help you organize these materials and build a comprehensive case summary that serves as your foundation for negotiations.

When DIY Makes Sense (And When It Doesn’t)

Before diving into negotiations, you need to honestly assess whether DIY settlement negotiation is right for your situation. Self-representation typically works best for cases with clear liability, medical bills under $6,000, minor to moderate injuries, and cooperative insurance companies. If you’re comfortable reading insurance documents and the fault is obvious, handling the claim yourself could save you attorney fees.

However, certain situations call for professional help. Complex liability disputes, serious injuries requiring ongoing treatment, medical bills exceeding $10,000, disputed Uber insurance coverage periods, or uncooperative adjusters usually benefit from attorney involvement. The FTC’s guidance on hiring lawyers suggests getting a consultation when your potential recovery is substantial or the legal issues are complicated. Remember, both paths are valid choices, and there’s no shame in starting DIY and switching to attorney representation if things get overwhelming.

Countering Low Offers With Facts, Not Feelings

When an insurance company makes an offer that seems too low, respond with specific medical findings, documented functional limitations, and clear treatment plans rather than emotional arguments or round numbers pulled from thin air. Request the adjuster’s valuation notes in writing and address each concern with records like imaging reports, specialist recommendations, or employer verification of missed work. Set a reasonable timeline for response and be prepared with next steps, whether that means invoking your own uninsured motorist coverage, escalating within the insurance company, or consulting with an attorney about your options.

Practical Steps If The Insurance Offer Seems Too Low

When you receive an offer that feels too low, instead of accepting immediately due to financial pressure or rejecting it out of frustration, here’s what to do if the insurance offer is too low after your Uber accident: take a methodical approach that strengthens your position and opens the door for productive negotiation.

- Request the adjuster’s written valuation breakdown and ask specifically how they calculated medical expenses, lost wages, and pain and suffering—this reveals exactly where they see weaknesses in your claim.

- Gather missing documentation to address their concerns, such as updated medical records, specialist reports confirming your diagnosis, or employer verification of your actual wage loss and missed shifts.

- Add any overlooked expenses like prescription costs, medical equipment, transportation to appointments, or childcare expenses while you recovered—these often get missed in initial reviews.

- Obtain a brief letter from your treating physician outlining your current limitations, expected recovery timeline, or need for future care—doctors’ letters often move offers higher.

- Submit a detailed counteroffer with your additional documentation, explaining how the new evidence supports a higher settlement amount, and set a reasonable timeline for their response (typically 10-14 days).

- Prepare your next options before you counter, whether that means escalating within the insurance company, exploring uninsured motorist coverage if applicable, or consulting with an attorney for a free evaluation of your case strength.

- Turn the case over to an experienced lawyer who can enforce the claim and pay zero upfront fees.

Uber Accident Settlement FAQs

When you’re dealing with an Uber accident, practical questions about money, timing, and your options feel urgent. These answers address the most common concerns about settlement amounts, who pays what, and whether you can handle negotiations yourself.

Who pays my medical bills while the claim is pending, and what if I can’t afford follow-up care?

Your health insurance typically pays upfront, then seeks reimbursement from the settlement. Many medical providers accept liens, meaning they wait for payment until your case resolves. If you’re worried about ambulance bills or ER copays, start with ZAF’s free assistant to understand your payment options and avoid treatment gaps that could hurt your claim.

How long does it take to receive a settlement after an Uber accident?

Simple cases with clear fault and minor injuries might settle in 2-4 months. Complex cases involving serious injuries, disputed liability, or multiple insurers can take 6-18 months or longer. Treatment completion and having all health records ready typically speed up the process significantly.

What factors influence the average Uber accident settlement amount?

Injury severity and medical documentation carry the most weight in settlement calculations. Most settlements range from a few thousand dollars for minor injuries to six figures for serious cases, but your specific situation matters more than any average. Strong evidence, such as photos and witness statements, insurance coverage limits, and fault percentages, all impact final offers.

Does it matter if I was the Uber passenger, the Uber driver, or in another car?

Your role determines which insurers might pay and how much coverage is available. Passengers generally have the strongest position with access to multiple insurance sources. Drivers face more complex coverage depending on their app status. Other drivers rely primarily on the at-fault party’s insurance and their own coverage.

Can I negotiate my Uber accident settlement without a lawyer?

Yes, many people successfully negotiate their own settlements, especially for straightforward cases with clear documentation. ZAF’s AI assistant can help you understand the process and build a case summary. Large or complex cases with moderate to serious injuries usually work better with an attorney, but the choice is yours.

What should I do if the insurance offer after my Uber accident seems too low?

Request the adjuster’s written valuation and address weak points with additional treatment records or wage documentation. Counter with specific facts about your injuries and treatment rather than emotions. If negotiations stall, you can consult with an attorney or explore other coverage options like uninsured motorist benefits.

Will filing a claim raise my own insurance rates if I wasn’t at fault?

Filing a not-at-fault claim typically won’t increase your rates, but policies vary by state and insurer. If you’re concerned, get clarity on your situation before proceeding. Most people find that protecting their right to compensation outweighs potential rate concerns, especially when they weren’t responsible for the accident.

Your Next Step: Get Clarity Today—At No Cost

Uber accident settlements depend on injury severity, insurance coverage periods, and how well you document your case. Focus on building a strong file with medical records, wage loss proof, and clear liability evidence. Whether you handle negotiations yourself or work with an attorney, organized documentation moves faster than emotion.

You have real options that don’t require upfront costs or pressure tactics. Start by understanding where you stand and what the claims process actually involves. AI tools are increasingly helping accident victims with intake and demand letter preparation, giving you clarity on your situation before deciding your next move.

ZAF’s AI-powered legal assistant for Uber accident claims helps you assess your situation, understand the insurance process, and build a case summary you could use as a settlement demand. From there, you can continue on your own, request a free consultation with a licensed attorney, or choose full-service representation with zero upfront fees. ZAF provides legal information and guidance, not legal advice, following established ethics standards for AI assistance in legal matters.

Get started with ZAF Legal to understand your claim and explore your options without cost or commitment.

This content is for informational purposes only and does not constitute legal advice, and that reading the content does not create an attorney-client relationship.

This material is provided strictly for informational and guidance purposes and does not constitute formal legal advice; furthermore, reviewing this content does not establish an attorney-client relationship.